Supermarket businesses have been experiencing a period of robust growth in recent years, creating optimism for the sector’s future, according to the 28th edition of the “Panorama of Greek Supermarkets” by BOUSSIAS Editors. However, profitability remains low, with all costs—operational and otherwise—continuing to rise.

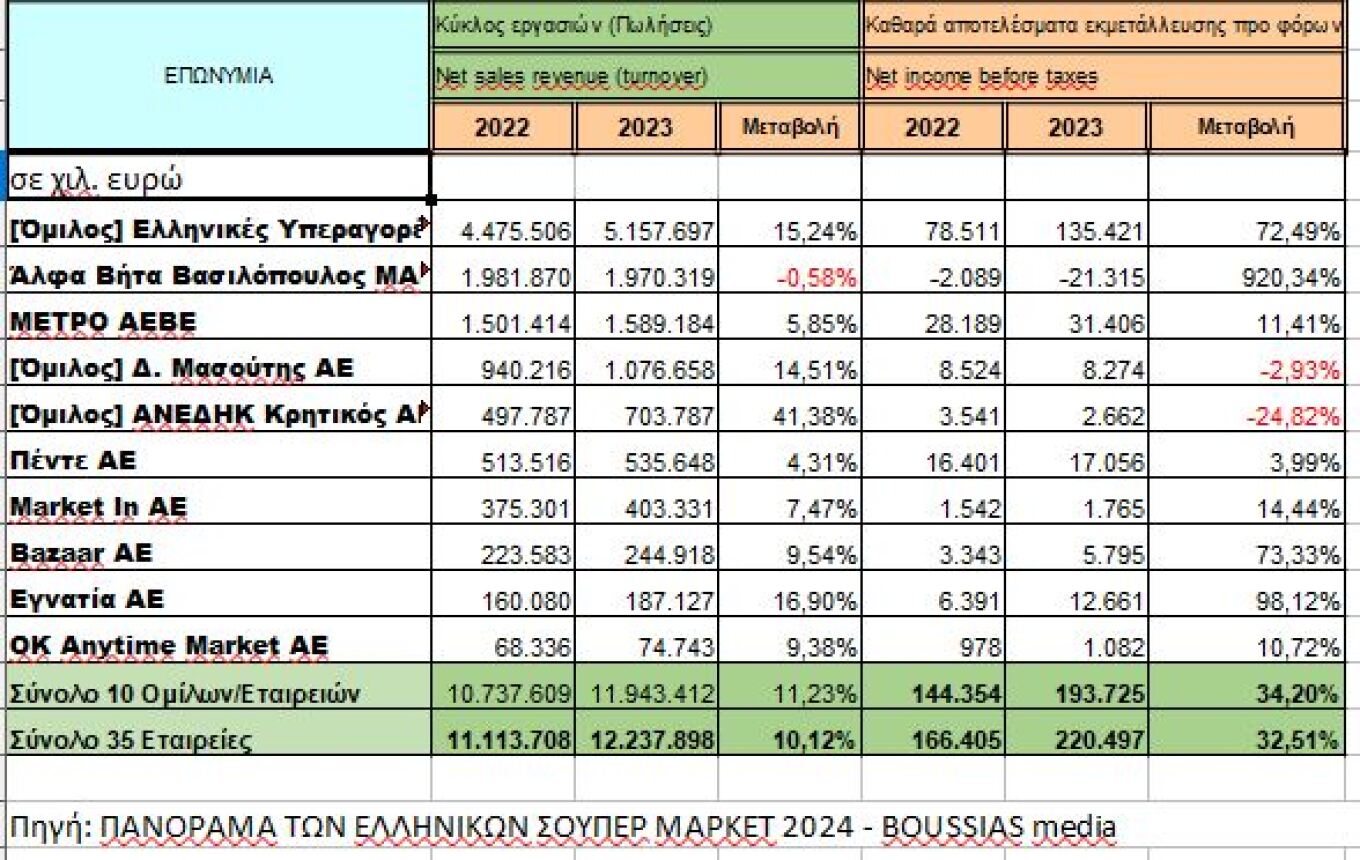

The data from this year’s Panorama of Greek Supermarkets is drawn from the financial statements of the 35 largest companies in the sector, excluding Lidl Hellas, which does not publish its financials. In 2023, these companies achieved sales of €12.24 billion, an increase of €1.12 billion or 10.12% compared to 2022. This marks the seventh consecutive year of significant sector growth, with sales increasing by 61% or €4.65 billion during this period. The surge is attributed to the pandemic and lockdowns, the full reopening and expansion of the former Marinopoulos network under Greek Hypermarkets Sklavenitis (GHS), the sector’s organic growth against competing networks, and inflation since the second half of 2021.

The special edition examines the key financial metrics of the ten largest companies by sales in 2023. The highest sales—and the largest growth in the sector—were recorded by the GHS group, totaling €5.16 billion, a 15.24% increase over 2022 or €682.19 million. Alpha Beta Vassilopoulos secured second place with sales of €1.97 billion, slightly down (-0.58%) from 2022. Metro (My Market and Metro Cash & Carry) came in third with a 5.85% sales increase and an annual turnover of €1.59 billion. The D. Masoutis group followed with a significant sales rise of 14.51% and a turnover of €1.08 billion. AΝEDIK Kritikos showed the highest percentage growth among the top ten, with a 41.38% annual sales increase and a turnover of €703.78 million, thanks to significant acquisitions in 2021-2022. Northern Greece’s Egnatia demonstrated the second-largest sales growth, up 16.9% to €187.13 million.

Pente ranked sixth with a 4.31% annual increase and a turnover of €535.65 million. Following it were Market In, with sales of €403.33 million and a 7.47% revenue increase, Bazaar, with €244.92 million in sales (up 9.54% from 2022), and OK Anytime with €74.74 million in sales, a 9.38% increase.

Collectively, the top ten groups and companies reported increased profits in 2023, returning to 2021 levels. They posted total pre-tax net results (profits) of €193.73 million, a 34.2% increase compared to 2022 but below the 2021 figure of €200.69 million. Consequently, the net profit margin for the “top ten” stood at 1.62%, compared to 1.34% in 2022 and 2.03% in 2021. The net profitability of all 35 companies in the sample was slightly higher, at €220.50 million compared to €166.41 million in 2022, translating to a sector net profit margin of 1.80% in 2023 versus 1.50% in 2022.

The gross profit margin for the top ten groups and companies remained stable at 26.91%, compared to 26.84% in 2022. It is noted that Law 4903/2022 “froze” profit margins for essential goods at August 2021 levels. Operating costs increased by 6.74% in absolute terms due to rising sales but decreased as a percentage to 23.3% from 24.28% in 2022. Financial costs, however, rose to 1.30% from 1.03%, resulting in a reduced operating profit margin (EBIT before financial costs) of 2.61%, down from 3.61% the previous year, aligning with typical sector levels.

The return on equity followed a similar trend. For the top ten groups and companies, it shifted from 11.42% in 2022 to 14.39% in 2023, while for all 35 companies, it increased from 11.91% to 14.88%.

The substantial sales growth in 2023 led to a proportionately smaller increase in liabilities to suppliers. Combined with a rise in current assets, this resulted in improved overall liquidity. Immediate liquidity also increased. The overall liquidity ratio rose from 63.27% to 67.35%, reaching satisfactory levels (it had dropped to 56.94% in 2020). Immediate liquidity improved sharply from 27.61% to 32.21% (it was at 27.09% in 2020).

Ask me anything

Explore related questions