The government seeks to rein in the practices of insurance companies, which, over the past three years, have inflated prices on health insurance policies by up to 45%, and now, some are beginning to increase property insurance rates for natural disasters in the wake of the 20% reduction in property tax (ENFIA) for insured properties. This is happening because the battle against inflation risks being lost in the services sector, where prices continue to soar as companies “inflate” their profits.

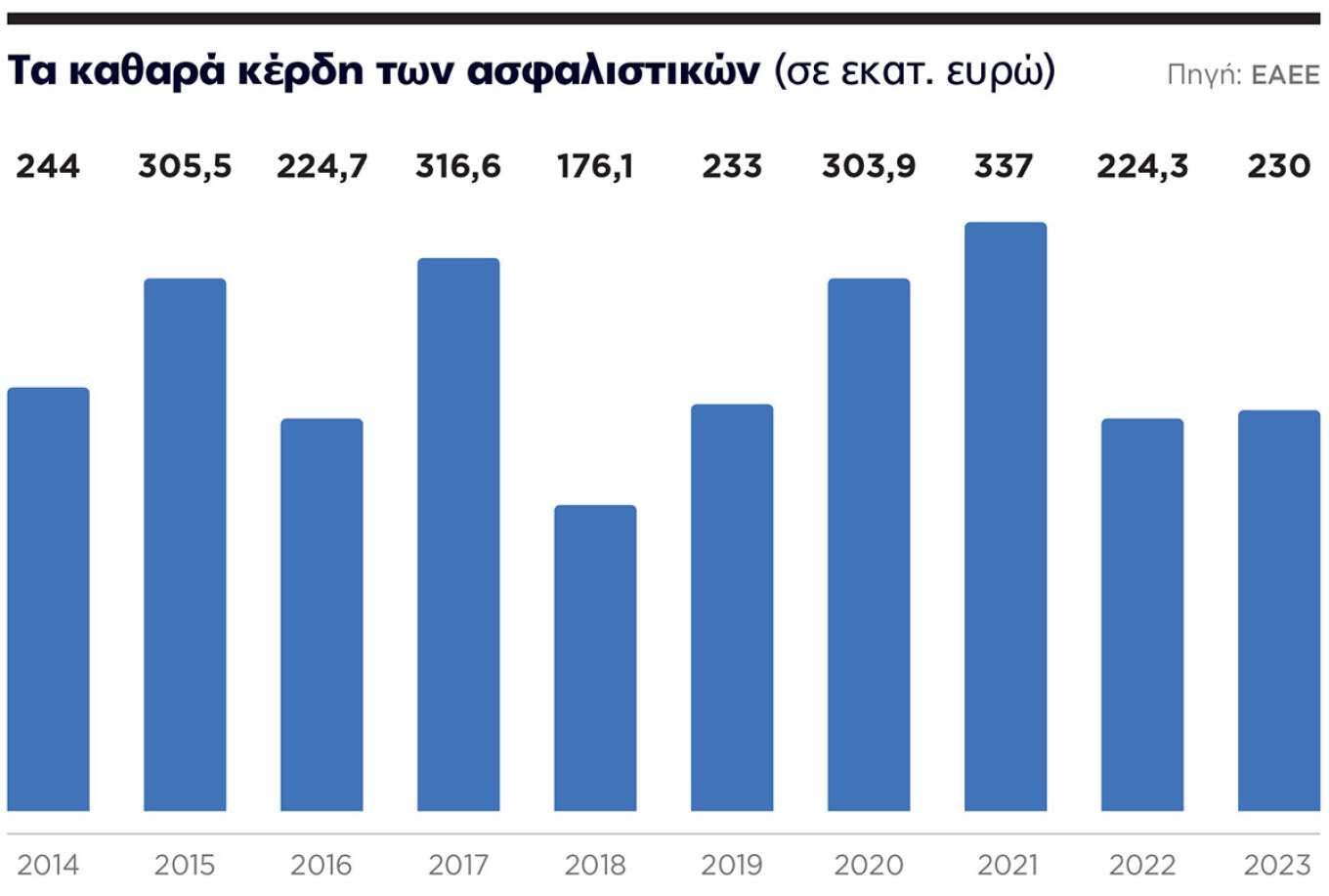

Specifically, in the last three years, the net profits of insurance companies have reached €780 million. This context also includes the legislative intervention announced last Friday by the Minister of Development, Takis Theodorikakos, which will address the large problem of the massive hikes in health insurance premiums, and his warning to insurance companies to “withdraw or not activate” the major price adjustments they have announced for their customers, both in lifetime and annual health insurance policies, totaling over 950,000 contracts. Instead, there will be discussions for a single-digit adjustment. Otherwise, as he told THEMA, a strong government intervention will follow, potentially even imposing price caps.

Minister of Development, Takis Theodorikakos

Investigation into Clinics

At the same time, the investigation into private hospitals launched by the Competition Commission is nearing completion, to determine whether there is a competition issue keeping prices high, as insurance companies allege.

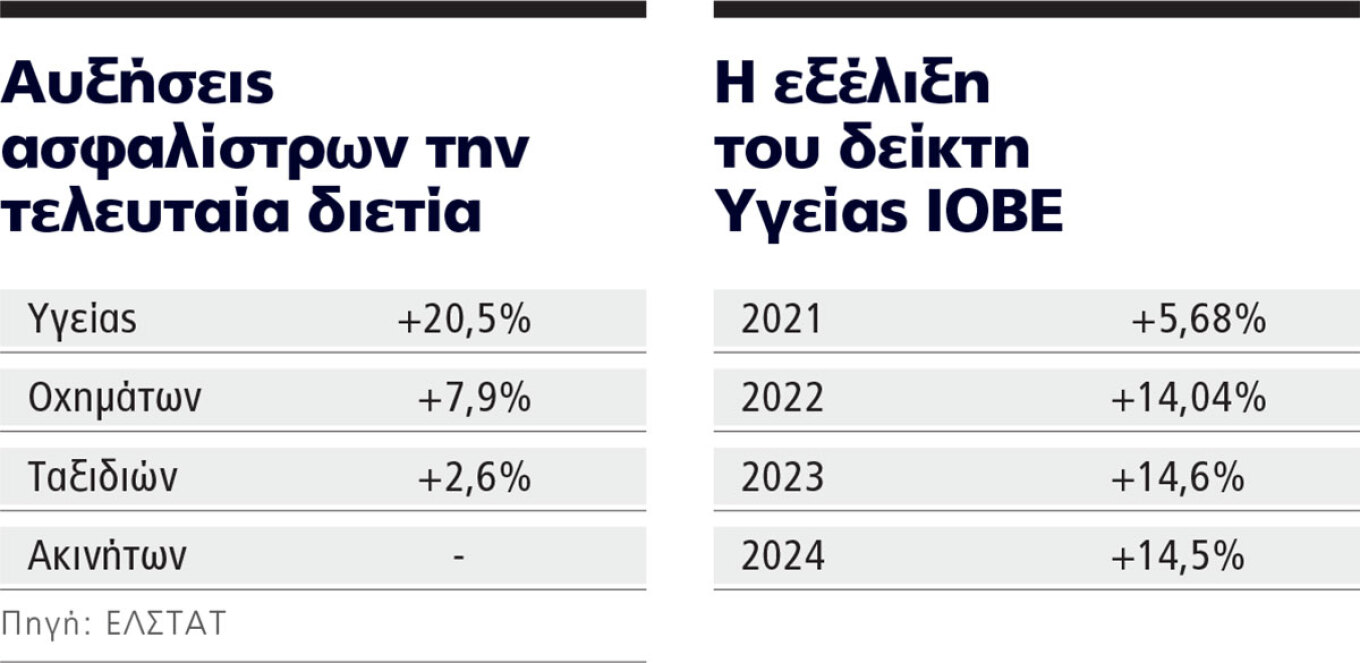

The legislative intervention, which will be prepared by the relevant ministries of Development, Finance, and Health, and after consultation with the Bank of Greece and the Competition Commission, will have as its central change the abolition of the IOBE Health Index as the basis for price increases in lifetime life and health insurance policies, which currently number 255,000. This is the index that led to health insurance premium hikes of 20% last year for lifetime contracts and about 9% for annually renewable ones, with 15% and 8% hikes announced for this year, respectively!

Starting from 2026, as announced by the minister, a new index will be prepared and enforced by the Hellenic Statistical Authority, which will operate similarly to a private health services inflation index, and all future price adjustments will be based on this. According to information, there will also be consideration of extending this new index to cover annual contracts to prevent a phenomenon where increases are moderated in lifetime contracts, while annual contracts rise disproportionately—essentially just shifting the already increased costs for the insured!

According to the Ministry of Development leadership, changing the basis on which premium increases will be justified will bring significant changes, reducing the current 15% annual cost increase, which was based on a complex formula developed by IOBE, factoring in not only the cost of services in private hospitals and the height of reimbursements but also the age of insured individuals, all of which were based on data provided by the insurance companies themselves.

The insurance companies are “passing the ball” to private clinics, accusing them of increasing health expenditure due to innovative surgeries and hospitalization, of unjustified overpricing, and of providing services provocatively, complaints that are being investigated by the Competition Commission.

Comparatively, in 2023, the Health Index compiled by ELSTAT, which primarily concerns price changes in public institutions where charges are different, was at +3.55%, while in 2022 it was 5.61%!

The abolition of the IOBE Health Index and its replacement with one from ELSTAT is a public admission that the last regulation introduced by the Ministry of Development in 2020, which legalized the relevant index, allowing insurance companies to act unilaterally, was wrong.

In fact, both the Scientific Committee of Parliament and the Consumer Ombudsman had warned clearly about the complications this could cause, especially about the fact that insured individuals would be left unprotected against the whims of companies that were supposed to reduce their exposure to costly old lifetime policies, a move that ultimately helped their profitability, which in 2023 was €230 million, in 2022 €224.3 million, and in 2021 €337 million.

According to information, the legislative intervention that will be prepared will also include the mandatory disclosure of critical data from all insurance companies to create a price observatory, where every citizen can check the prices of basic policies by category.

In fact, the Ministry of Development intends for the observatory to apply to every insurance sector, so there is overall transparency, allowing consumers to easily compare. It is believed that this will further boost competition, as has happened in the vehicle insurance sector with the operation of digital price comparison platforms.

What the Insurance Companies Want

From that point on, there will be a round of consultations to explore other actions that could lead to interventions aimed at reducing the cost of insurance policies. For their part, insurance companies, through the Union of Insurance Companies of Greece, have already submitted a memorandum with five proposals directed at the relevant ministries to address the issue.

First, strengthening competition in the healthcare sector by simplifying the framework for creating new private hospitals. Second, the broad implementation of diagnostic-related groups (DRGs) in the private sector, regardless of who pays (EOPYY, insurance companies, private individuals).

In other words, a price list for every procedure. Third, a review of the high 24% VAT rate on private healthcare services. Fourth, the extension of the exemption of health insurance premiums from a 15% tax to all ages or at least for those over 65 years old (the government had previously established a tax exemption for insuring minors). And fifth, a Public-Private Partnership (PPP) through collaboration between insurance companies and public hospitals for the benefit of citizens, policyholders, and state revenue.

Increases in Home Insurance

While the main issue may focus on health insurance contracts today, there are voices calling for interventions and safeguards regarding the price adjustments made by insurance companies in other categories of insurance. Recently, the following phenomenon has been observed: one by one, companies have been announcing adjustments to their premiums for home insurance contracts against natural disasters.

This started being recorded immediately after the government’s announcement of a measure to incentivize citizens to insure their properties against natural disasters by offering a 20% reduction in property taxes (ENFIA) for insured properties, which clearly shows the companies’ intention to benefit from the incentive established by the government. A short-sighted move that ultimately undermines “insurance faith” by not taking seriously the significant prospects now opening for the industry.

The leadership of the Ministry of Development, however, has stated that this issue will also be examined, referring to possible legislative measures that will be prepared. The legislative initiative announced by PASOK for the market is eagerly awaited, given that the situation with skyrocketing health insurance premiums is now causing political debates.

And not without reason, as in the last three years, there has been a tectonic shift in the market, especially concerning health insurance contracts, where companies are clearly steering policyholders towards annually renewable contracts, in which they believe they are free to adjust premiums and benefits every year without any limitations. It is estimated that each year, about one in eight policyholders is forced to cancel their private health insurance, with exorbitant increases in old contracts creating a clear shift toward the cheaper option of annual contracts, which, however, provide fewer benefits and reimbursements.

In 2018, lifetime contracts numbered 350,000. According to official figures from the Hellenic Association of Insurance Companies (EAEE), by 2023, they had decreased to 255,000, while approximately 740,000 contracts are renewed annually. However, old contracts account for the majority of reimbursements. Specifically, of the total reimbursements of 483 million euros paid in 2023 for individual health insurance contracts, 50%—specifically 240.1 million euros—went to lifetime insurance programs!

These are the old hospital programs, i.e., those sold from the 2000s to 2015, which also included life insurance, meaning lifelong coverage. Because they were complementary programs to the basic lifelong life insurance, these programs are called “lifetime” and the insurance company cannot withdraw them from the market. The vast majority of insurance companies have, in fact, stopped selling such programs.

Hospital Coverages

The increases in insurance premiums for both categories have become a permanent tug-of-war between policyholders and insurance companies and are attributed to the high reimbursements that insurance companies are obligated to pay each year for hospital coverages, which account for 94% of the cost of reimbursements.

Insurance companies blame private clinics, accusing them of increases in healthcare costs related to innovative interventions and hospital stays, unjustified overpricing, and providing unnecessary services, such as numerous tests that are sometimes irrelevant to the disease, in order to increase hospitalization costs.

The situation in the healthcare services market is currently being monitored by the Competition Committee to determine whether the changes in the market have led to any competitive complications. On the other hand, representatives of private clinics reject the insurance companies’ claims, stating that the increases in the price lists they notify to insurance companies have not exceeded 3% this year.

They also point to significant delays in their payments, which in most cases exceed one year, reaching up to 18 months! They also accuse insurance companies of placing a cap on innovative interventions.

In any case, the reality is that there are numerous distortions in the private healthcare system, which are also reflected in the latest annual report from the Health Care Cost Institute, which places Greece among the most expensive countries in Europe for a series of surgical procedures. According to the report, the average cost of a gallbladder surgery in Greek private hospitals is charged to insurance companies at 7,713 euros, whereas the corresponding cost in Switzerland is 7,948 euros, in Spain 3,510 euros, and in Germany 6,508 euros.

The list of discrepancies is long, and among them are treatments such as appendicitis surgery, which costs 6,860 euros in Greece, compared to 6,992 euros in Switzerland, 2,136 euros in Spain, and 3,796 euros in Germany. The report describes other common medical interventions and their average costs. For example, a coronary bypass with cardiac catheterization (the number of hospital days covered by insurance ranges from 18 days to 10 days) costs 32,400 euros in Greece, just slightly higher than in Switzerland (32,000 euros), compared to 17,000 euros in Germany and 13,800 euros in Spain.

Regarding the average cost for a coronary angioplasty in a private hospital, Greece is once again in the same position as Switzerland, at 9,183 euros, while in Spain the cost is 8,280 euros and in Germany only 3,658 euros. For hip replacement surgery, Switzerland is more expensive (15,615 euros), but the cost in Greece (10,200 euros) remains higher than in Germany (7,292 euros) and Spain (6,638 euros).

A cesarean section in Greek private hospitals costs 5,881 euros, compared to 7,668 euros in Switzerland, 3,573 euros in Germany, and 2,712 euros in Spain. Similarly, a natural birth in Greece costs 4,659 euros, in Switzerland 5,436 euros, in Germany 2,361 euros, and in Spain 1,774 euros. For cataract surgery that does not require an overnight stay, Greece leads in price with 2,636 euros, Switzerland follows with 1,832 euros, Germany with 790 euros, and Spain with 1,740 euros.

Complaints

However, the unfair practices employed by many insurance companies are evident from the increasing complaints filed by consumers with the General Secretariat for Consumer Protection, the Consumer Ombudsman, and consumer organizations such as EKPOIZO (Consumers’ Union Quality of Life). Some “brave” individuals will also take legal action, but with the pace at which the justice system operates, this creates a hostile environment.

“The complaints against insurance companies received by the Consumer Ombudsman have increased dramatically, with the main request being the inspection and cancellation of abusive premium increases. At the same time, there is a trend among insurance companies to gradually abandon lifetime life insurance policies and replace them with annual contracts,” the Consumer Ombudsman states in the 2023 annual report, which was presented to the Speaker of the Parliament a few months ago.

According to EKPOIZO, the main issues and complaints from consumers relate to the adjustment of premiums, with the most notable being the situation with lifetime health contracts, the lack of pre-contractual information from certified insurance intermediaries (mainly for investment and pension programs), the refusal of compensation with pretextual arguments, and unfair commercial practices misleading consumers regarding offered programs.

According to the Union, “insurance companies often use pretextual arguments so that consumers are not compensated for the coverage of surgical procedures or diagnostic tests. For example, they frequently argue that the materials used in procedures are not included in the list of covered benefits, resulting in compensation for only part of these, even though the insured person had initially informed about the procedure without the insurance company raising any objections. They also provide verbal pre-approval only to later revoke it after the procedure, etc.”

The Consumer Ombudsman, among the successful mediation cases during the year, mentions the case of compensating an insured individual for a gynecological procedure, which the company delayed under the pretext of requiring a medical examination that did not actually exist.

In the same context, many companies implement exclusions from new health insurance when the insured person reaches a certain age limit. For example, in a case known to “THEMA”, a 55-year-old who had already completed 30 years on a health contract, with minimal use of the policy, was effectively excluded from renewing it because his high blood pressure and elevated cholesterol prevented coverage for basic health issues like cardiovascular problems!

Also, according to EKPOIZO, it is a common phenomenon, especially in investment and pension programs, the lack of pre-contractual information from certified insurance intermediaries. This policy results in consumers not being fully informed about the terms and content of the contract, as well as the future risks involved.

The organization also denounces the phenomenon of selective insurance. In a relevant case that reached “THEMA”, an insured person who wanted to insure their house in an area recently affected by a fire could not do so, as most companies had frozen any procedures for that area for at least six months!

Vakakis’ Outrage

Another critical issue is the charges imposed after a compensation claim. A notable example involves insured homes and businesses affected by the natural disaster “Daniel” in Thessaly last year. While the insurance companies compensated the victims, later, according to complaints, they demanded exorbitant increases for renewing the coverage, which attracted public attention when the well-known businessman and major shareholder Apostolos Vakakis expressed his outrage during a general assembly regarding the increases demanded by the insurance consortium to conclude the new contract.

Among the complaints EKPOIZO has reported, one case stands out: an insured person since 2011, whose premiums for their health insurance contract have reached nearly 2,200 euros annually from 950 euros in the first year. Another insured person complains in a letter about the 22.6% increases to their lifetime contract in the previous two years. A third person reports that at the end of 2023, while they were admitted to a private clinic for surgical treatment and knew that the insurance company covered 80% of the cost and the remaining 20% was covered by EOPY, they were asked to pay 55% of the total cost, which amounted to approximately 17,000 euros, while the insurance company paid 40%.

Ask me anything

Explore related questions