A unique standoff is currently unfolding in Greece’s housing market between property owners and prospective buyers. Buyers are adopting a wait-and-see attitude, hoping that prices will eventually come down, while sellers continue to hold firm and maintain high expectations. The result is a sharp slowdown in new transactions, with far fewer deals being completed than in previous years.

Although data from the Bank of Greece still show residential property prices rising in the first quarter of 2026, the pace of growth has slowed considerably compared to 2025. Real estate professionals, however, paint a different picture. They report that asking prices have largely stabilized and, in some cases, have even begun to decline. According to Lefteris Potamianos, President of the Athens-Attica Association of Real Estate Brokers, prices remain very high and are unlikely to experience any dramatic correction, but the market is no longer seeing meaningful increases because transactions have become scarce. Many of the sales being finalized today were already in progress last year, while current listings often reflect sellers’ overly optimistic expectations rather than actual market demand.

Market sentiment has also been affected by geopolitical uncertainty and its economic consequences, particularly the ongoing crisis in the Middle East. Combined with already elevated prices, a shortage of new housing supply, and a large number of unused properties, uncertainty is making buyers more cautious.

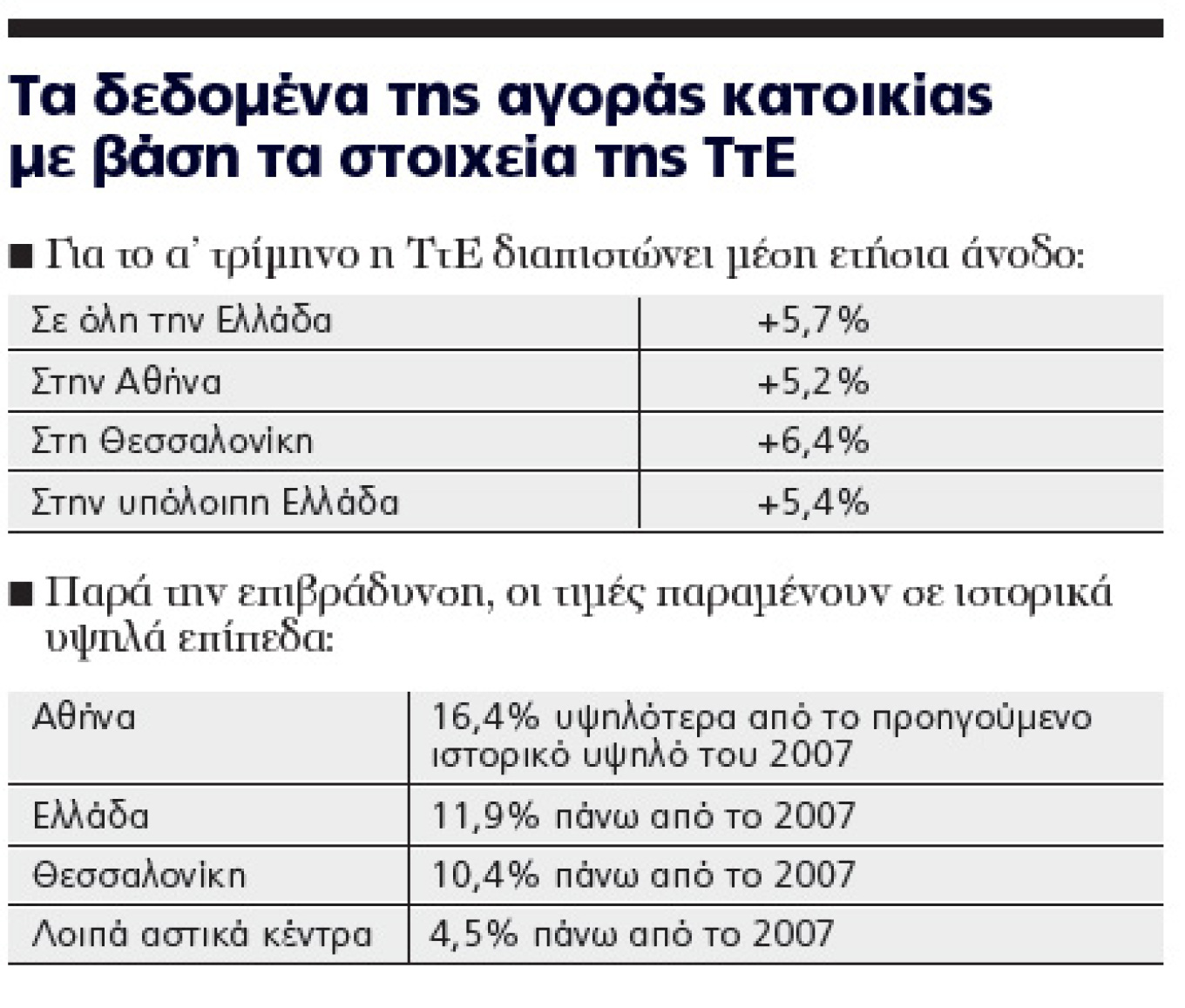

Official figures from the Bank of Greece show that nationwide residential property prices rose by 5.7% year-on-year during the first quarter of 2026, compared with 8.3% in the previous quarter and 8.1% during 2025 as a whole. In Athens, annual growth slowed to 5.2%, lower than the 6.4% recorded in Thessaloniki and the 5.4% recorded in the rest of the country. The data also confirm that housing prices have now surpassed their pre-financial-crisis peak of 2007 by 11.9% nationwide. Athens leads the way, with prices more than 16% above their 2007 highs, while Thessaloniki is slightly above 10% and other urban areas approximately 4.5% above their previous peak.

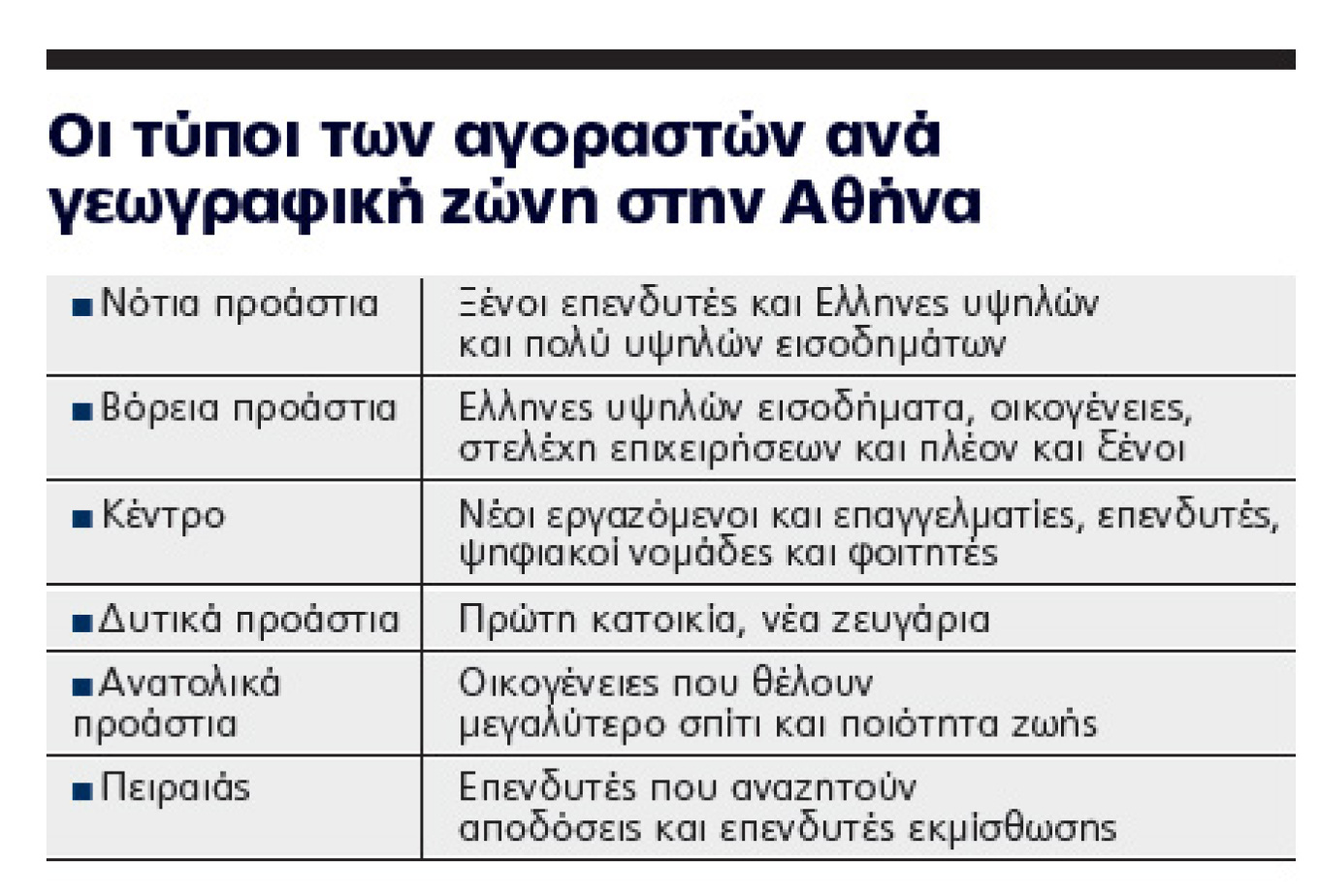

The sharp increase in housing costs over the past few years has created distinct buyer profiles across Athens. One of the most notable trends is the growing popularity of the western suburbs among young families and first-time buyers. More affordable prices, better value for money in terms of living space, a stronger neighborhood atmosphere, and improved metro connections to central Athens have made these areas increasingly attractive. Properties between 70 and 110 square meters, particularly renovated homes close to public transportation, are among the most sought-after. Areas such as Peristeri and Aigaleo are also seeing greater investment interest than in the past, while Aigaleo has become particularly popular for smaller apartments aimed at students.

In the eastern suburbs and the wider Mesogeia region, including areas such as Paiania, Pallini, and Spata, demand comes mainly from families looking for larger homes at lower prices than those found in more established family-oriented districts such as Chalandri or Marousi. Porto Rafti is increasingly being promoted as an affordable alternative for buyers seeking either a primary residence or a vacation home without paying the premium prices associated with the Athens Riviera.

The southern suburbs and the Athens Riviera continue to attract wealthy Greeks, foreign investors, corporate executives, members of the Greek diaspora, and some second-home buyers. According to market analysts, this is currently the most investment-driven region of Attica. Foreign buyers now account for a significantly larger share of demand, even in areas that traditionally appealed mostly to Greek households. Demand is strongest for newly built, energy-efficient homes with parking spaces, large terraces, and easy access to the coastline and the massive Ellinikon redevelopment project. Sustainability has become a key consideration for international buyers, with environmentally certified properties often commanding significant price premiums.

The northern suburbs remain the preferred destination for affluent households seeking quality of life, green spaces, security, and strong educational infrastructure. Areas such as Kifisia, Chalandri, Melissia, and Pefki continue to attract family buyers, while luxury districts like Psychiko and Filothei appeal to ultra-high-net-worth individuals. These neighborhoods have shown greater resilience than the broader Athens housing market and continue to command some of the highest prices in the capital. Marousi, meanwhile, is strengthening its position as Athens’ main business district, attracting executives and investors interested in modern, energy-efficient housing close to major office developments.

Central Athens remains the city’s most diverse residential market. Demand comes from young professionals, students, local residents, foreign buyers, and investors looking for rental opportunities. Smaller apartments, particularly renovated units close to metro stations, remain highly desirable due to their strong rental yields. Upscale areas such as Kolonaki, Mets, and Pangrati continue to attract higher-income buyers, while neighborhoods like Kaisariani, Ilisia, and Ampelokipoi offer more affordable alternatives. Foreign buyers, including digital nomads, are increasingly exploring these districts as lower-cost options compared with central premium neighborhoods.

Piraeus has also emerged as a major investment destination. Urban regeneration projects and opportunities linked to the Golden Visa program have increased interest from foreign buyers, especially non-EU investors. Demand focuses largely on renovated apartments suitable for long-term rentals, while nearby Moschato is gaining popularity thanks to redevelopment projects along the Faliro waterfront.

Overall, the Attica housing market appears to be entering a new phase. Prices remain historically high, but buyer resistance is increasing and transactions have slowed considerably. While major price declines are not expected, the market is becoming more selective, rewarding modern, energy-efficient, high-quality properties while making it increasingly difficult for older, less competitive homes to attract buyers.

Ask me anything

Explore related questions