International oil prices remained above $100 a barrel on Friday as the war in the Middle East approaches its third week, heightening concerns about prolonged disruptions to global energy supply.

Brent futures were trading at around $101.15 a barrel in early morning trading, up 0.7%, while U.S. West Texas Intermediate (WTI) crude was slightly higher at $95.87.

Despite a slight retreat from intraday highs, oil prices are on track for a second consecutive week of strong gains. Brent is up more than 9% this week, after surging nearly 28% the previous week—the biggest weekly increase since the pandemic in 2020. WTI, which posted its best weekly performance since 1983, is also heading for another weekly rise.

Investors continue to closely monitor developments in the Middle East, where the war involving the United States, Israel, and Iran appears to be expanding. U.S. President Donald Trump suggested that the conflict is unlikely to end anytime soon, stating that Washington has “unparalleled firepower, unlimited ammunition, and abundant time.”

At the same time, according to a report by Axios, the U.S. president reportedly told a conference call with G7 leaders that Iran is close to surrender. However, the country’s new supreme leader, Mojtaba Khamenei, responded via state television that Tehran will continue to fight.

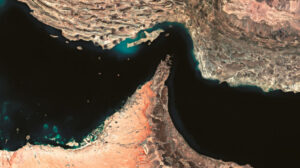

Meanwhile, several foreign ships in or near the Strait of Hormuz—one of the world’s most critical energy corridors—have come under attack in recent days, heightening fears of serious disruption to global oil flows.

A spokesperson for Iran’s military command, Ebrahim Zolfakari, warned that oil prices could climb as high as $200 a barrel if regional security continues to deteriorate.

Prices remain elevated despite efforts to stabilize markets. The International Energy Agency has agreed to release a record 400 million barrels from strategic reserves, while the White House announced a temporary easing of some sanctions on Russian oil exports.

Analysts at Barclays note that investor anxiety is rising, as markets had initially priced in only a short-lived conflict.

At the same time, EnQuest chief executive Amjad Bseisu said the oil market is facing a crisis of unprecedented scale. According to him, each day of delayed restoration of normal supply removes about 20 million barrels from the market, intensifying pressure on prices.

He added that the last time the global market experienced a similar contraction in supply was during the Arab oil embargo of the 1970s, when prices nearly quadrupled.

Ask me anything

Explore related questions