The reform of Greece’s tax administration is one of the most important but least publicized changes of the post-crisis period, according to a new analysis by the International Monetary Fund (IMF).

The IMF describes Greece’s transition from a system characterized by low tax collection efficiency, political interference, and widespread tax evasion to a more independent, digitized, and effective tax administration model.

The report argues that this reform has played a crucial role in fiscal stabilization and in restoring the credibility of the Greek economy, while noting that the next challenge is the use of data technologies and artificial intelligence to make the new system permanent and even more efficient.

The three phases of the reform

1. The crisis period: stabilizing revenues and fighting tax evasion

The first phase begins with the outbreak of Greece’s sovereign debt crisis in 2010, when the state’s inability to collect taxes had become a major factor in fiscal instability.

According to the IMF, the priority during this period was the immediate increase of revenues and the fight against systemic tax evasion. Special units were created for large taxpayers and high-net-worth individuals, high-risk audits were strengthened, and more systematic monitoring of overdue tax debts was introduced for the first time.

The Fund notes that during this phase the focus was mainly on emergency measures aimed at preventing a collapse in public revenues.

2. Institutional restructuring: the creation of the Independent Authority for Public Revenue (AADE)

The second phase concerns the deeper institutional reform of the tax system. The IMF highlights the creation of the Independent Authority for Public Revenue (AADE) as a key development, granting greater administrative and operational autonomy from political leadership.

According to the report, AADE’s independence enabled greater continuity in reforms, improved strategic planning, and a more professional tax administration. At the same time, collection procedures improved, risk management was strengthened, and more targeted tax audits were introduced.

The IMF places particular emphasis on the gradual shift away from a fragmented and politically vulnerable tax administration system.

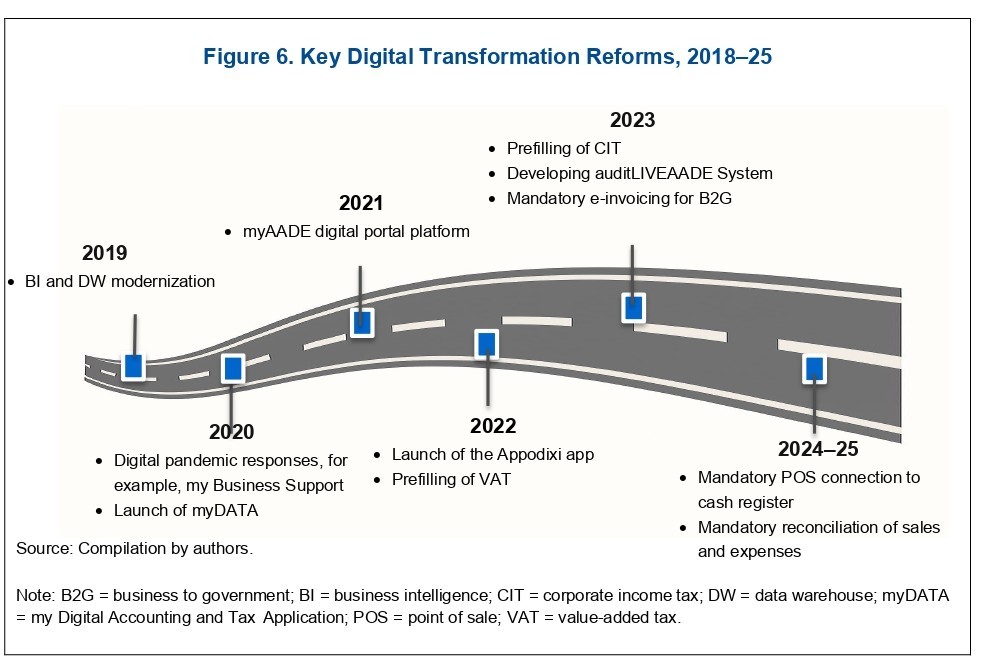

3. Digital transformation: from manual checks to real-time data

The third phase is the digitalization era, which the Fund considers decisive for improving tax compliance.

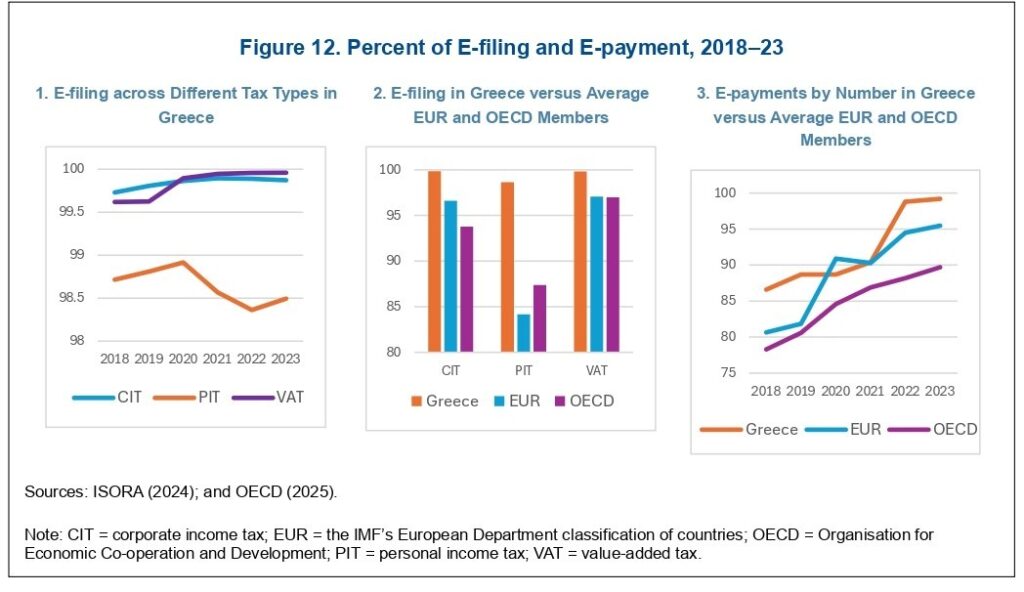

The expansion of electronic payments, the interconnection of POS systems and cash registers, electronic invoicing, and the myDATA platform have created—according to the report—a new environment in which economic activity is recorded with far greater accuracy and speed.

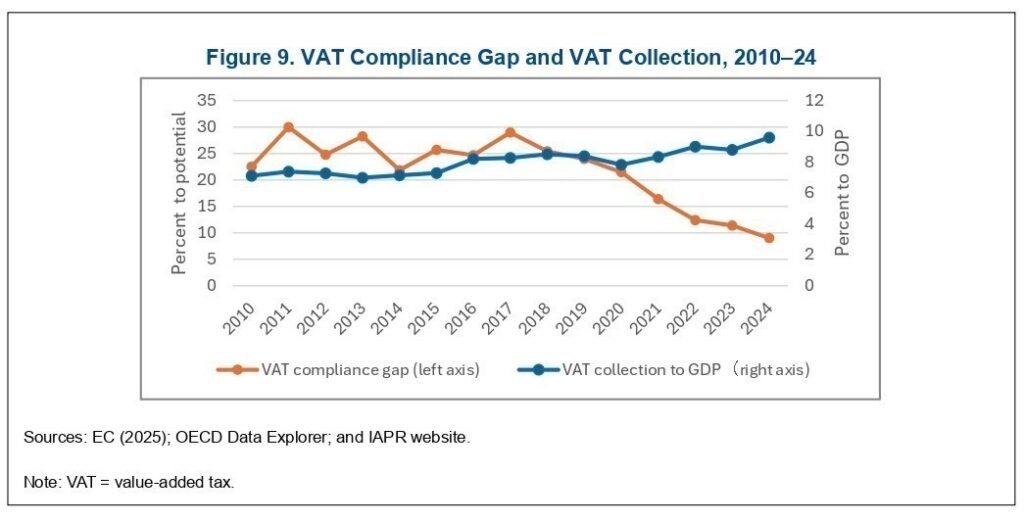

The IMF notes that digital tools have enabled AADE to move from mass but often inefficient audits to more targeted interventions based on data analysis. This shift is closely linked to the significant reduction in the VAT gap and improved tax collection efficiency.

The next step: a data- and AI-driven tax authority

In the final part of the analysis, the IMF argues that Greece’s tax reform is now entering a new phase, where the main objective is no longer just revenue collection but the creation of a permanently efficient, technology-driven tax system.

Strategically, the Fund emphasizes strengthening data analytics and the responsible use of artificial intelligence, fully integrated into tax risk management systems. This, it says, would enable a shift from reactive audits to preventive compliance management.

The report highlights that the growing availability of data through myDATA, e-invoicing, and POS integration now allows for near real-time monitoring of economic activity. However, the challenge is to systematically turn this data into operational decisions.

For this reason, the IMF recommends integrating data analytics and AI tools into core tax administration functions, from audit selection to debt management and dispute resolution, ensuring decisions are driven by data rather than used only as supplementary input.

At the same time, the report stresses that technology alone is not enough. The sustainability of the reform depends heavily on strengthening staff skills, developing leadership capacity, and improving human resource management. The new model, it notes, requires greater expertise in data analysis, digital systems, and risk management.

The IMF also emphasizes that the next phase should place greater focus on taxpayer service and trust in the tax system. As compliance becomes more automated, issues such as transparency, fairness, and easy access to services will become increasingly important for voluntary compliance.

A more taxpayer-centric approach—supported by integrated digital services, simplified procedures, and pre-filled tax returns—can reduce compliance costs, limit errors, and strengthen trust in the system, IMF economists note.

Finally, the Fund states that continued progress will depend on good governance, realistic planning, and effective resource management.

It concludes that the tax administration should continue evolving toward a more integrated, digital, and reliable “Tax Administration 3.0” model based on data and technology.

Ask me anything

Explore related questions