IMF warns Europe: Public debt could surge to 130% of GDP by 2040 without action

A new International Monetary Fund (IMF) study warns that Europe needs deep structural reforms and fiscal adjustment, as rising public spending threatens the long-term sustainability of government finances

Newsroom

Δείτε περισσότερα άρθρα μας στα αποτελέσματα αναζήτησης

Europe’s public debt trajectory risks becoming unsustainable unless governments take immediate and meaningful steps to stabilize their public finances, the International Monetary Fund (IMF) warned in a study published on Monday.

The IMF’s economists argue that the piecemeal approach adopted by many European countries has reached its limits, as fiscal pressures intensify due to population ageing, the energy transition, rising defence spending, and persistently weak economic growth.

The study, authored by Luc Eyraud, Mahika Gandhi, Andrew Hodge, Giacomo Magistretti, Ian Stewart, Mengxue Wang, and Jiaye Yu, warns that unless long-term spending pressures are addressed in time, public debt in many European countries could follow an “explosive trajectory.”

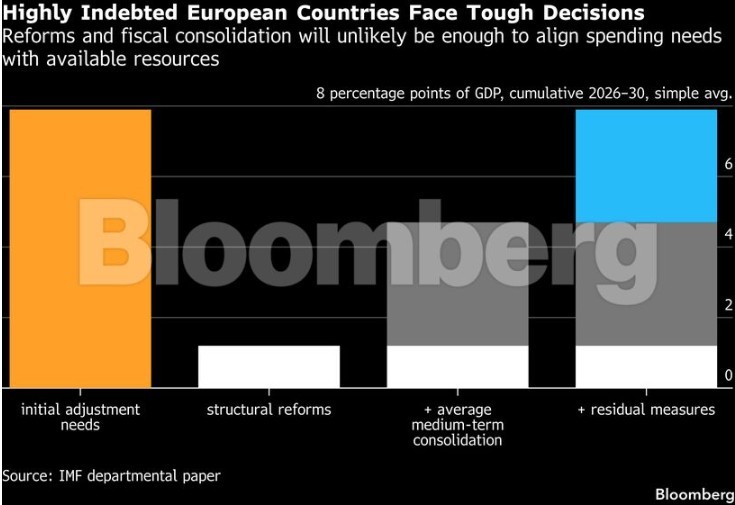

“If long-term spending pressures remain unaddressed, debt dynamics could enter an explosive path in many European countries. Small-scale measures are insufficient given the scale of the adjustment required and could even lead to reform fatigue,” the IMF economists wrote.

The warning adds to a series of recent reports highlighting the fiscal vulnerability of several European countries more than a decade after the sovereign debt crisis that threatened the stability of the euro area. Particular concern now surrounds countries such as the United Kingdom, France, and Belgium, where public debt has reached or exceeded the size of annual economic output.

The IMF urges governments to move away from short-term fixes and adopt a longer-term strategy.

“Governments need to pursue a more deliberate and forward-looking strategy that combines structural reforms, fiscal consolidation, and, where necessary, deeper decisions regarding the scope and financing of public services. As the cost of delay rises, the benefits of a strategic approach become increasingly evident,” the report states.

Debt could reach 130% of GDP by 2040

According to the IMF’s projections, public spending across European countries will increase by nearly 5% of GDP on average by 2040, at a time when economic growth is expected to remain subdued and political willingness to raise taxes or implement major spending cuts is likely to be limited.

Without substantial policy action, average public debt could climb to around 130% of GDP, roughly double its current level, putting public finances on an unsustainable path.

The study estimates that a moderate package of structural reforms could close about one-third of the fiscal gap, with the greatest benefits coming from pension reforms and policies aimed at boosting economic growth.

However, the IMF stresses that fiscal adjustment will also be necessary in most countries.

“Both reforms and fiscal consolidation are typically required, and both involve difficult political decisions. The greater the progress on reforms, the smaller the need for fiscal adjustment. However, relying solely on reforms will not be sufficient to address risks to fiscal sustainability.”

Possible changes to the welfare state

For countries with particularly high public debt, the IMF suggests that even more far-reaching measures may be needed, including a reassessment of the range of services provided by the state.

According to the report, rethinking the role of government does not necessarily mean shrinking the public sector or dismantling Europe’s social model. Rather, it calls for a realistic assessment of which services are best financed by the public sector, which could be delivered more efficiently or equitably with greater private-sector involvement, and how responsibilities should be allocated.

The study notes that extensive social welfare programmes, universal public healthcare, and free education have been key drivers of economic growth, social cohesion, and political stability in Europe since the Second World War. Nevertheless, it argues that today’s fiscal environment may require parts of that model to be reconsidered.

The IMF also highlights examples of countries where such discussions are already underway. Austria and Croatia are reviewing public-sector wage costs, while Belgium, France, and Norway are exploring ways to better target social spending. Meanwhile, Germany, Slovakia, and Turkey are seen as having significant scope to reduce broad-based energy subsidies.

The report concludes with a warning that fiscal policy choices will become increasingly constrained, politically contentious, and consequential, adding that the fragmented and reactive approach many countries have followed so far has reached its limits.