Hello, the military operations in the Middle East continue, the Americans and the Israelis claim they are close to the full “defensive exhaustion” of Iran, and that may well be the case. It seems that the regime of the mullahs being unable to even minimally counterattack is probably near; what no one predicts or even estimates with any reliable indications is the next day in Iran. Let’s first see who the interlocutors of the West will be, analysts say, because the rate at which they are being physically eliminated is high. Otherwise, the markets are reacting rather calmly; of course oil prices have surged, but it is still early for conclusions. Athens is closely monitoring all developments, Mitsotakis is speaking with everyone he needs to speak to, and for the time being the country is handling the crisis properly. Of course, K.M. was not quite as much of a tough guy as the socialist Sánchez who, as soon as Trump slightly bared his teeth at him, sent his very best frigate—but what can you do. If nothing else, he disappointed everyone from Haris Doukas to Dimitris Avramopoulos, who declared that “the Spanish prime minister stood up to the U.S.”, but in the meantime the Spanish prime minister had not heard him on Greek TV and sent the ship anyway. In general, however, in the last few hours there has been a silence from “The Bitter Ones S.A.—Antonis Samaras, Kostas Karamanlis (Rafina) and Co., formerly New Democracy.” I hear from colleagues that the first days of polling show a “surge” for Mitsotakis and the government due to the war crisis; it seems logical to me but temporary, though not without significance. People always “record” on their hard drive that there is stability and responsibility in the stance of a prime minister, and even his opponents “grant” Mitsotakis that he has a certain institutional demeanor and steadiness in his views. Among other things, I also read yesterday Karystianou’s statement on the events and although it was a sympathetic statement—“we demand a world without wars…”—it reminded me of something like Yoko Ono and the Beatles’ “imagine all the people living life in peace.” What can you comment?

Mitsotakis–Macron

-We may be hearing it from the French, but I understand that the Mitsotakis–Macron phone call was quite interesting regarding the solution the French are looking for on the security of navigation in the Red Sea and then in Hormuz, where things are clearly more difficult. Because as time passes insecurity hits the economy, the Europeans are “looking around,” in communication with the Americans as well, for such a difficult region. Macron in the call with K.M. referred specifically to the case of Suez, but it is interesting that at this moment he has called both Athens and Rome. In any case, even the thought of this has quite a few operational difficulties, from the situation on the ground to who would have overall command, but exploratory contacts are taking place.

In Paris

-Since I’m mentioning Macron, let me remind you that K.M. has a scheduled trip next Tuesday to Paris to participate in the Summit on nuclear energy convened by the French president. He will go as planned, unless the geopolitical balances in the region change drastically, in which case he might also have a one-on-one with Macron, who under normal circumstances will come to Athens after Easter for the renewal of the Greek-French defense cooperation.

Papastavrou–Samaras

-I wrote to you in recent days, on the occasion of Samaras’s “attack” on the government over the contracts with Chevron, that it is interesting that the attack also catches one of his own people, Energy Minister Papastavrou. Until a few months ago Papastavrou was trying to act as a “channel” between the government and Samaras, but I understand that lately the relations between the two have also worsened. In this context I listened with interest yesterday to the Environment and Energy Minister from Parliament responding to the criticism over the Chevron contracts, saying that the contractual provision even for extreme cases—and therefore the safeguarding of the State—is a standard legal practice that does not mean acceptance or recognition of such cases.

EKCOMED–TV Channels

-An interesting discussion (sic) is currently unfolding around the allocation of the resources of EKCOMED, which constitute basic “fuel” for the TV channels. I remind you that every year roughly one third of the money goes to subsidizing series on the six private channels and two thirds to series on platforms and foreign productions filmed in Greece. Last year, the package for the private channels was 20+ million euros and was distributed equally. This year, however, channels that do not have series in their programming (SKAI, Star, Open) are trying to bring shows or reality programs into the equation as well. Obviously, the subsidy criteria are determined by the Ministry of Culture and EKCOMED, and there is generally “good will” along the lines of: why, for example, shouldn’t SKAI’s Voice or Star’s Master Chef be programs eligible for subsidies? I understand, of course, that the complications begin in the case of Open, which is also interested, since it does not produce series but has essentially fully assigned its entertainment programming to Koklonis, who still has some tax and legal pending issues. If the subsidy criteria “open up,” in any case, the devil will be in the details of the wording. Note that I, as a commentator of good intentions, called the whole matter an “interesting discussion.” Someone else might call it an “interesting transaction,” because, after all, elections are coming too, right?

Odysseas–Adonis–Sánchez!

-A major brand is the PASOK MP from Arcadia Odysseas Konstantinopoulos, but these New Democrats don’t have… a clue either: all together they have set out to drive Androulakis crazy. Konstantinopoulos made a post that was institutional and serious and scolded the supporters of the “heroic” Spanish socialist Sánchez. Adonis picked it up and publicly… praised him while denouncing the hypocrisy of the Left regarding the Spanish Prime Minister. I remind you here that Georgiadis and Konstantinopoulos have had an excellent relationship since the time they were at the Ministry of Development, as minister and deputy minister respectively, during the Samaras–Venizelos coalition government. I also remind you that Odysseas had warmly supported Haris Doukas in the internal party elections, but that did not prevent him from fully distancing himself from the left-leaning outbursts of the mayor of Athens in favor of Sánchez. The first muddle is created in PASOK, and immediately afterward the government spokesman Pavlos Marinakis comes to… tie the knot. He reminded that Spain “has chosen to arm a country that maintains an active casus belli outside any logic and international law against a country that is a member of the European Union and NATO, which is Greece,” something that “the domestic ideological doubters also pretend to forget, because they put their ideological obsessions above the interests of their country,” and concluded: “What I say, perhaps even better than I say it, was also said by the Vice President of Parliament and PASOK MP, Mr. Konstantinopoulos.”

When the offers for Lavrio open

-The hearing of the appeals filed with the Council of State regarding the concession of the port of Lavrio was moved to the end of the month, as the procedure the day before yesterday was postponed. The case is very interesting because apart from concerning a large project involving the upgrade of the third largest port in Attica, there is the following unusual element: the appeals were not filed against the Superfund but among the participants in the tender. Specifically, appeals were filed by the consortium Olympic Marine – Cruise Terminal Investment (Prokopiou Group and MSC) and Jet Plan Shipping (interests of Marios Iliopoulos) and, as sources close to the process said, they essentially concern the legality of each other’s participation—namely whether the file is complete, whether the proper supporting documents exist, etc. The other schemes that passed to the second phase were GEK TERNA – CELESTYAL, INTERKAT (Papaioannou Group) – Beaufort Sea Shipping Corporation – Newsphone (Theodosis – Apergis), and Israel Shipyards Industries. If the tender clears the judicial-legal issues, the binding offers can be unsealed by the Superfund and within the next one to two months the preferred investor could be selected. For the Lavrio Port Authority, the intention is the sale of at least 50% of the share capital plus one share.

Superfund: Barrage of tenders

-On the occasion of what we said above about the port of Lavrio, let us add that G. Papachristou of the Superfund—after going through a period during which he placed suitable people from the private sector on the boards of the supervised companies—has mobilized the forces of the Superfund to attract investments. Just during this period the tender is running for the development of the Saltworks, where nine investors have appeared. At the same time, the tender is moving forward for Tatoi, in which five interested parties declared their presence, while an additional four investment schemes expressed interest in the tender for the concession of cruise activity at the ports of Katakolo, Patras and Kavala. Also another eleven investors appeared for the 129-acre property in Posidi in Halkidiki, while the procedures are also advancing for the leasing of beaches in Attica.

Which area of Athens has the most expensive houses

-Which is the area where almost 1 in 2 houses is now sold for over 1 million euros? It is not the southern suburbs, where prices may have soared even above 25,000 euros per square meter for isolated cases of residences right on the sea. Based on data from the digital real-estate platform Prosperty and publicly available figures from the tax authority, the highest ratio of expensive houses is found in Palaio Psychiko. Specifically, according to the company’s data, the houses for sale in the Palaio Psychiko area total 367, with an average price of 6,500 euros per sq.m. The few villas in P. Psychiko currently on the market—just nine—are sold at an average price of 10,400 euros, while for detached houses, 118 in number, the corresponding figure reaches 7,600 euros per sq.m.

Raid for cryptocurrency scams

-A team from the Hellenic Capital Market Commission traveled yesterday to Crete to assist the Greek FBI in the operation to dismantle a criminal organization involved in cryptocurrency scams. The Greek FBI had been monitoring the specific case for quite some time, until yesterday when the combined raid by the authorities took place, leading to 12 arrests. The raid was carried out simultaneously in Rethymno and Heraklion.

Well, well, it’s coming…

-It is a fact… “Barry’s is making its appearance in Athens. Make sure to sign up to the list to be informed about exclusive memberships before opening, events and much more!” This is stated on the official page of the famous American gym chain Barry’s, which now hosts the announcement for the Greek “branch.” With Tyler McBeth in the starring role, as the column has already informed you in time. Although adventurous at first, the business venture of Stefanos Kasselakis’s husband is now entering the final stretch. Of course, there are still no available dates, as it seems that the opening is placed around the end of the month or sometime in April. Barry’s Greece was initially to be housed on Kanari Street in Kolonaki, but the case went sideways and a new location was sought, which was found on Syntagma Square in a building on Othonos Street. In other words, it doesn’t get more… central than that. Of course, that also has the corresponding price in terms of rent, which information places at around 20,000 euros monthly. In any case, everything shows that Tyler will do just fine since the memberships will also be… of a corresponding level, while with all the buzz that has been created he won’t be able to keep up with the clientele. In any case, the brand is smashing it both in America and in many other countries, as it has evolved into one of the most sought-after boutique fitness studios in the world. “Barry’s is not a fitness trend. It is science and it works. It is the global destination to enjoy the best workout of your life,” as it introduces itself. For the record, Barry’s Bootcamp (now known as Barry’s) was founded in 1998 in the heart of West Hollywood by Barry Jay and John and Rachel Mumford, launching pioneering high-intensity interval training classes in a group environment. A central element of the whole project is the Red Room, a space with red lighting, loud music and many treadmills. In 2011 the brand conquered New York and in the same year the first studio outside the U.S. opened in Bergen, Norway. In the following years spectacular growth followed both in America and abroad, in London, Dubai, Milan, Stockholm and many other major cities, now counting more than 85 locations. Well, it was Athens’s turn too… via Tyler.

The kiss of life for Greek Real Estate

-The bombings in the Middle East and the Iranians’ asymmetric threats are proving to be powerful fuel for the surge of the Greek real estate market. Every new round of tensions in the region turns Greece into the closest, safest and most welcoming place a well-off resident of Tel Aviv, Beirut or Istanbul could imagine. It is a trend that has been recorded in the past, but it is now gaining new momentum. According to the annual survey of RE/MAX Greece for 2025, Israelis now constitute the majority of foreign buyers in Attica. Turkish and Lebanese investors follow. Israelis also hold first place in property transactions in Thessaloniki. Data from the Bank of Greece confirm that inflows of Israeli capital for real estate purchases reached €129 million in 2024, up +46.5% on an annual basis, with total Israeli investments already estimated at over €700 million. Today they have already conquered the €1 billion stronghold. Israelis with a residence card in Greece more than doubled in just one year: from 661 in 2024 to 1,355 in 2025, an increase of 105%. Turks are investing in Greek real estate at a pace of €300 million per year and in December 2025 they held second place in Golden Visa permits, behind only the Chinese. Security, climate, political stability and prices that remain 20 to 30% lower compared with similar markets in the Mediterranean are the strong points of Greek real estate. The cost of living in Greece is 25–30% lower, the flight lasts less than four hours, and the Golden Visa opens the door to Europe.

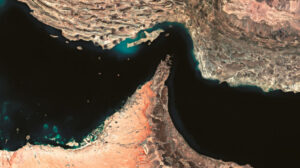

Greek shipping as a barometer of risk in the Strait of Hormuz

-At a time when the international shipping community is keeping its distance from the dangerous waters of the Persian Gulf, one Greek company appears to be taking up the challenge. Dynacom Tankers Management, according to information from international platforms that track ship movements, sent five vessels through the Strait of Hormuz into the Persian Gulf at a time when passage has nearly frozen due to the war conflict. In practice, this strategy is old Greek shipping school. Risk, timing and geopolitical reading. The fewer ships that enter the Gulf, the greater the bargaining power for those who do. And we are not talking about a small fleet. The passage included the suezmax vessels Pola and Smyrni, as well as three LR1 product tankers, Kerala, Kavomaleas and Athina. It is not the first time that Greek interests have stepped forward into difficult seas. From the Persian Gulf to the Black Sea, Greek shipping has proven that it often functions as the market’s barometer of risk. The picture in the region resembles a wait before a storm. Dozens of tankers have anchored in the Gulf of Oman and the Arabian Sea, carrying capacity equivalent to more than 500 million barrels of oil. Most shipowners prefer to wait.

K. Konstantakopoulos and the capital discipline preferred by the NYSE

-In the containership market the most interesting moves are not always the ones that make noise, but those that reveal strategic thinking. And the latest move by Costamare of Kostis Konstantakopoulos appears to be exactly that. The company, listed on the New York Stock Exchange, added four newly built containerships of 3,100 teu to its orderbook, increasing the capacity of its orders by 12,400 teu. At first reading it is simply another investment in the fleet. On second reading, however, it is a move that resembles more the logic of a Wall Street investor than that of a traditional shipowner. The ships belong to the feeder category, a segment of the market that serves the major hub ports and usually offers more stable demand and long-term charters. It is no coincidence that all ten vessels Costamare currently has under construction, the six it ordered last year and the four signed recently, already have secured employment before delivery. In other words, the company is expanding its fleet without taking pure risk on the freight cycle, but with revenues “locked in” for years. This approach, which reduces exposure to market volatility, is exactly the type of capital discipline American investors prefer. The message being sent to the market is clear. Costamare is not chasing the next shipping boom, but gradually building a base of predictable cash flows in a segment with structural demand. And in a market that remains deeply cyclical, this “quiet” strategy is often the one that proves most resilient over time.

The moves of the Greeks who read the market

-Restrained but absolutely targeted, according to financial analysts of the shipping market, is the activity of Greek shipowners in the second-hand vessel market this week. The lists of second-hand sales did not record Greek purchases in dry bulk, containerships or gas carriers, with interest concentrated almost exclusively in the tanker market, confirming that Greeks continue to see prospects in this specific segment. The most characteristic was the purchase of the Suezmax STENA SUNSHINE (159,039 dwt, built in 2013 at Samsung Heavy Industries shipyards in South Korea), which according to information passed into Greek hands for around $63.5 million. The vessel is equipped with a scrubber and an eco main engine, elements that analysts note make it attractive at a time when energy efficiency and emissions regulations play an increasingly important role in investment decisions. At the same time, Greek interests also appeared on the sellers’ side. The product/chemical tanker TIGRIS (12,920 dwt, 2009, STX Offshore & Shipbuilding) was sold to buyers based in the United Arab Emirates for approximately $9.6 million. In dry bulk, two Supramax vessels changed hands: KAPTA MATHIOS (58,743 dwt, 2009, Tsuneishi Zhoushan) which headed to Chinese buyers at about $13.75 million and THEODORA (53,569 dwt, 2008, Iwagi Zosen) which was sold for around $13 million to buyers not yet disclosed. At the same time, Greek shipowners remained active in the newbuilding market. In the crude oil sector Cape Shipping ordered a VLCC with capacity of 319,000 dwt at CSSC Beihai Shipbuilding in China, with delivery in 2029. In the LNG sector Tsakos Energy Navigation secured an LNG carrier with capacity of 174,000 cubic meters with an option for another, at Samsung Heavy Industries shipyards in South Korea, with a reported price of about $255 million and delivery in 2028.

The next “bloodbath” in the IT sector

-The major projects of the Recovery Fund are coming to an end and the attention of IT companies is turning to the next major investments of the Greek state in digital transformation. One project that is set to evolve into a major thriller in the coming days, weeks and months is the new National Critical Wireless Communications System (MCNGR) with a budget of €90 million, which may reach €180 million (including option and VAT). On March 29, 2026 the public consultation for the tender documents of the international competition will be completed, which will be conducted by the National Infrastructures for Research and Technology Network S.A. (EDYTE). The knives, however, have already come out of their sheaths. The object of the project is the design, development and operational function of a unified national system of critical wireless communications for the personnel of the Hellenic Police, the Hellenic Coast Guard and other Security Corps and competent agencies operating in the field and contributing to security operations, search and rescue missions and border management. The new unified system will make use of alternative radio-network technologies, existing infrastructure, satellite and VHF/UHF solutions, ensuring full geographic coverage of the territory (land, sea and air) to transmit voice, image and data.

Water in the spotlight

-The share of EYDAP (+0.94% at €8.63) is heading rapidly toward a market capitalization of €1 billion following the Paulson–Peristeris deal. A further rise for the share of EYATH (+1.06% at €3.83), which reaches €140 million, but more impressive is the rise in the price of UNIBIOS (+3.52% at €3.52) which with a market capitalization of just €40 million sees its dreams becoming reality. Water is becoming the absolute protagonist in the Middle East as well. Everyone talks about oil prices, very few deal with water, the truly vital element in the Middle East. Kuwait obtains 90% of its drinking water from desalination plants. Oman, 86%. Saudi Arabia, roughly 70%. Across the entire Arabian Peninsula the population drinks water produced from the sea. There everyone fears a bombing attack not on an oil well, but on desalination infrastructure. Here in Europe, technologies in this sector are evolving rapidly and the issue concerns governments and local actors. The investment interest expressed for the seemingly “negligible” 9.71% stake in EYDAP will now also be transferred to other companies related to the sector.

The big opportunity for refineries

-Motor Oil (+3.03% at €35.42) and HelleniQ Energy (+1.72% at €8.7) stand out like a fly in the milk in this stock market turmoil. It is not only international oil prices that increase refining margins and profitability due to the revaluation of inventories. There is another important detail. Jet fuel, the fuel used by aircraft, saw its price more than double. From $30.8 per barrel on Friday, February 28, it soared above $70 within 72 hours. The warplanes of the United States and Israel are flying nonstop and need special fuels. It is a fact that Motor Oil and HelleniQ Energy appear to be benefiting in the short term, as inventories acquired at lower prices gain higher value, creating a positive impact on their profit margins. But that is not all. Motor Oil has the highest yield in aviation fuel of any refinery in the Mediterranean. It has made investments of more than €200 million in this sector. A corresponding advantage is also created at HelleniQ Energy, which has worked on the fuel mix since the distant past, when aircraft with piston engines used high-quality aviation gasoline (avgas) in combination with lubricating oils (motor engine oil) to ensure operation under extreme conditions.

New jobs from DYPA in Business Parks

-DYPA — the former OAED — has moved into a new era and instead of benefits it offers training opportunities and well-paid jobs. It signed a memorandum of cooperation with ETVA VIPE aiming to provide paid apprenticeships to 22,500 young people (aged 16–29) throughout Greece. These young people will be trained in DYPA schools across the country in specialties that exist in ETVA’s Business Parks. Jobs that correspond to the real needs of industry. ETVA has created a special platform so that industries established in the Industrial Areas can select the specialties and number of people they need based on the available specialties, while if there are specialties not foreseen they will be created according to the needs of industry ad hoc. They will be paid from the first day and will have both education and practical training. Costs will be covered by DYPA. In this way, an organized effort is being created — for the first time — to build a dynamic industrial “blue collar” workforce. Times are changing and modern specialties in industry pay up to 40% more than an office job.

The end of the era for technical analysis?

-Stanley Druckenmiller is a Wall Street trader who became known for his correct market positions which were largely based on technical analysis. In a television interview he stated that today the effectiveness of technical analysis has been reduced to 20% compared with 30 years ago. Back then, nobody used it. Today everyone uses it. Therefore, there is no comparative advantage or uniqueness in the reaction. Today Druckenmiller is forced to return to fundamentals. What truly matters is buying healthy companies and avoiding paying excessively for them. As Peter Lynch used to say, in the long term the price of a stock will follow the financial results of the company, regardless of the “drawings” on a chart. The real advantage of the analyst is understanding businesses and their prospects.

War is bombing Americans’ wallets

-During the election campaign, President Trump had promised that he would bring the cost of gasoline down to $2 per gallon (one gallon, 3.8 liters). Today that campaign promise is collapsing with a bang. U.S. crude oil (WTI) yesterday exceeded $78 per barrel, up +43% since December. Since the beginning of January, diesel futures have surged by +56% to $3.29 per gallon. The corresponding gasoline futures contracts are moving +48% higher at 251 cents. The national average for unleaded reached $3.11 per gallon, with a jump of 11 cents overnight. This is the largest daily increase since March 2022. Goldman Sachs has already raised its forecast for Brent oil to $76 per barrel for the second quarter, with a scenario of $100 if the Strait remains closed for 5 weeks, while JP Morgan sees even $120. The United States is the largest oil-producing country in the world, but American crude is mainly suitable for gasoline, not for diesel, kerosene and heavier fuels. Therefore, the country depends on imports for these products, which explains the disproportionate rise in diesel futures. Higher oil prices mean higher freight rates, more expenses for aviation fuel, higher distribution costs and ultimately higher prices for the American consumer. At gas stations across America drivers remember the campaign promise of $2. $3.25 per gallon is the new reality.

Ask me anything

Explore related questions