A catalyst for reassessing the risks facing Greek and Cypriot banks is the new geopolitical crisis in the Middle East, bringing to the fore both the structural dependence on tourism and maritime and the macroeconomic vulnerabilities associated with energy and external deficits.

Two recent reports, from Morningstar DBRS and Autonomous, paint a more complex landscape: on the one hand, pressures on growth and asset quality are highlighted, and on the other, the impact of rising oil prices and widening spreads, with the common denominator being increased uncertainty for the banking sector. Despite the resilience that banks have shown so far, the evolution of the crisis will be the determining factor for their performance in the coming period.

Rising geopolitical tensions in the Middle East are bringing back into focus a critical and often underestimated risk for Greek and Cypriot banks: their high exposure to two key pillars of their economies—tourism and shipping. Despite strong profitability and capital buffers, the deterioration of the external environment is increasing risks to asset quality and the dynamics of credit expansion.

According to an analysis by Morningstar DBRS, Greece and Cyprus show a disproportionately high dependence on these two sectors, making them more vulnerable to external shocks compared to other European economies. The resurgence of the crisis in the Middle East, particularly the possibility of prolonged disruptions in shipping and air transport, is creating a more complex and uncertain environment.

Disruptions in transit through the Strait of Hormuz and the rerouting of shipping routes have increased transportation costs and risk insurance premiums, leading to higher freight rates. In the initial phase, this supports the revenues of shipping companies and, by extension, their ability to service loans.

However, this situation is not sustainable. Rising fuel costs, longer distances, and uncertainty in global trade may pressure shipping companies’ profit margins, gradually increasing credit risk for banks.

For Greek banks, exposure to shipping is high but characterized by diversification and asset-backed financing (secured by vessels), which limits immediate risks.

Tourism is the most direct transmission channel of risk

In contrast, tourism is the most sensitive link, as it is directly affected by geopolitical tensions. Flight cancellations, higher travel costs, and a deteriorating sense of security are already leading to cancellations and slower demand.

The impact is more pronounced in Cyprus due to its geographic proximity and greater dependence on specific markets such as Israel. In Greece, the effects are considered more manageable, as the country can act as a “safe alternative” destination compared to others, provided the crisis does not escalate further.

Nevertheless, the transmission of risk is clear: lower tourist flows affect the revenues of small and medium-sized enterprises, household disposable income, and ultimately loan quality.

Data from the European Banking Authority highlight the structural exposure of banks: loans to transport and storage account for 19.8% of business loans in Greece and 11.2% in Cyprus, compared to just 5.5% in the EU. Similarly, exposure to tourism (accommodation and food services) reaches 11.1% in Greece and 21.2% in Cyprus—multiple times the European average.

This high concentration increases banks’ sensitivity to sectoral shocks, although asset quality remains strong so far, with low non-performing loan ratios.

Macroeconomic impact and the road ahead

Initial downward revisions to growth forecasts have already begun. The Bank of Greece now estimates growth at 1.9% for 2026, down from 2.1%, incorporating the effects of increased geopolitical uncertainty and energy costs. Similarly, the Central Bank of Cyprus has reduced its GDP forecast to 2.7%, down by 0.3 percentage points, even under the assumption that the crisis will be relatively short-lived.

This is particularly important, as even under a “mild” scenario, growth is already being revised downward. In the event of prolonged tensions or further increases in energy prices, the scope for deterioration remains significant. At the same time, secondary effects such as higher energy prices, inflationary pressures, and potentially tighter monetary policy are creating a more challenging environment for banks—especially regarding loan demand and funding costs.

Greek banks show stronger short-term resilience thanks to their portfolio structure and solid fundamentals, while Cypriot banks are more exposed to immediate shocks. However, the evolution of the crisis will be the decisive factor. In a scenario of prolonged tension, pressures on tourism and shipping could shift from manageable to systemic, bringing asset quality concerns back to the forefront across the banking sector.

Autonomous: Oil hits the economy and banks

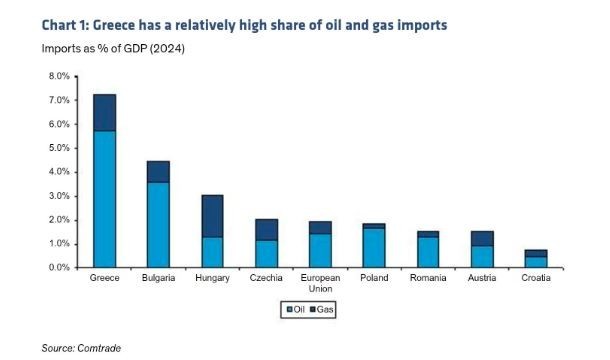

Greece is also considered vulnerable to higher oil prices, as it is a purely importing country.

This is highlighted in a report by Autonomous, which notes that the conflict in the Middle East has led to a decline in Greek bank stock prices.

“We assess that Greece is vulnerable to higher oil prices, with additional risk arising from the widening of government bond spreads due to an increased current account deficit. By contrast, the shipping sector does not currently appear to be a major concern.”

The firm issued a neutral recommendation on Piraeus Bank, as its valuation has become less attractive relative to other banks in the sector, while expressing a preference for Eurobank and National Bank, maintaining the same recommendation for Alpha Bank (negative).

Greece is a major importer of oil, which weighs on the current account balance, especially when prices are high. The deficit reached -5.7% of GDP in 2025, with a clear correlation to oil prices.

Although there is exposure to shipping, the risks appear manageable, as few vessels are directly affected and insurance coverage is in place. Additionally, higher freight rates have boosted the sector’s revenues.

Ask me anything

Explore related questions