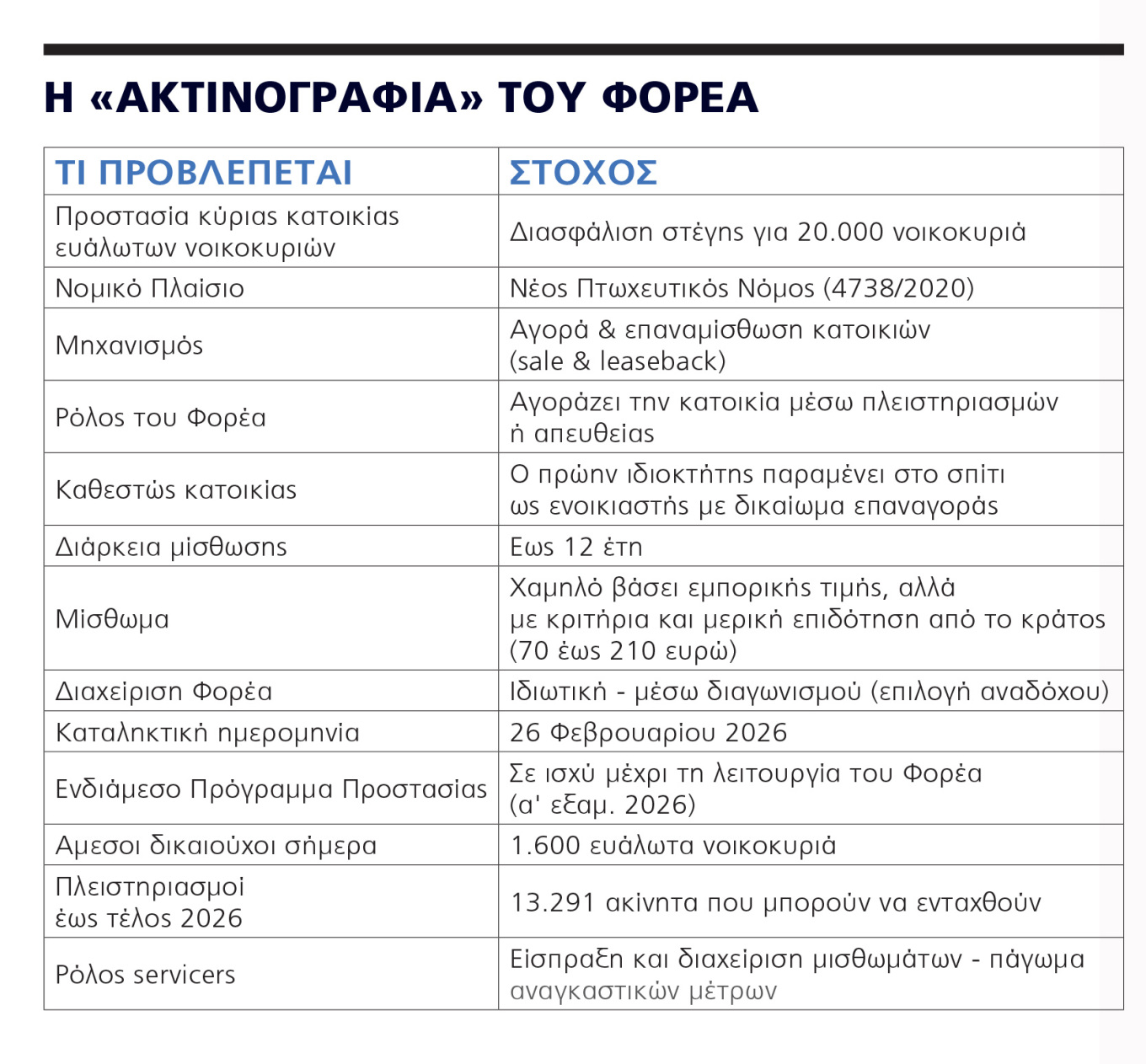

By the summer, the new institution of the Property Acquisition and Leaseback Agency is expected to become operational in Greece. This mechanism has been designed to provide a solution for more than 20,000 vulnerable debtors who have reached a definitive dead end, so that they do not end up homeless due to foreclosure or bankruptcy. The new “home-saving agency” intervenes so that the vulnerable borrower remains in their residence, if no longer as an owner, at least as a tenant, but with state subsidy and an option to repurchase it.

The basic architecture of the model promoted by Finance Minister Kyriakos Pierrakakis—and which will be implemented in Greece—provides for the creation of a private entity selected through an international tender. This entity will “buy” the primary residence of the vulnerable debtor before it is lost at auction, with the aim of leasing it back to the same person for 12 years. The lease framework grants the right to repurchase the home, provided the debtor recovers financially and proves consistent with their obligations.

In practice, “remaining in the home” is transformed into an institutionally guaranteed right. However, because this is a social policy tool—and not a general “umbrella” for everyone—eligibility requires cross-checks and verification through the vulnerable households certification platform, in order to prevent abuse.

Second chance to reclaim their home for those who lost it to banks and servicers

Finance Minister Kyriakos Pierrakakis, who is coordinating the creation of the new agency for the protection of vulnerable households

Who is eligible

With the launch of the binding bids phase for assigning the management of the agency, the Ministry of National Economy and Finance activates the mechanism aimed at preserving primary residences for borrowers hit by the economic crisis. The initiative combines private-sector participation with state support and aspires to become the ultimate safety net for the truly vulnerable.

More than 20,000 households in Greece meet the vulnerability criteria and are expected to seek inclusion in the program to avoid the sword of foreclosure through the Property Acquisition and Leaseback Agency, according to sources familiar with the scale of “potentially” impoverished households.

At this stage, even before the new agency is formally established and operational, the first beneficiaries expected to join immediately include more than 1,300 households that have applied via the special platform to obtain vulnerable household certification, as well as over 300 vulnerable households already receiving a monthly subsidy of up to €210 through the interim housing protection program, under which they were included so that servicers and banks would not threaten their homes.

In reality, many more people fall into this category—either out of ignorance or because foreclosure has not yet reached their doorstep—and have not yet taken the necessary steps to be officially declared “vulnerable.” However, by the end of 2026, 13,291 property auctions are scheduled, which is expected to mobilize those who have not yet made use of this provision.

How it will work

The project to establish the agency began in 2021. It is now nearing completion, as shortly before the end of 2025 the Ministry of National Economy and Finance announced the second and binding phase of the tender.

The Property Acquisition and Leaseback Agency is a key tool of the new Bankruptcy Law (4738/2020) and aims to support vulnerable households by allowing them to remain in their primary residence even after losing it due to bankruptcy. The mechanism is based on the international “sale and leaseback” model, adapted to the needs of the Greek reality. It provides the solution many borrowers have been seeking from servicers: staying in their home by paying rent instead of loan installments.

Step-by-step process

The first step for those wishing to join—often overlooked or neglected—is to obtain a vulnerable debtor certificate from the special platform of the General Secretariat for the Financial Sector and Private Debt Management.

Under current criteria, vulnerability for inclusion in the program requires: income of up to €7,000 for a single-person household or up to €21,000 for families with children, and property value not exceeding €120,000 (adjusted according to family members). Limits also apply to deposits and movable assets, in line with the Housing Allowance framework.

Once the borrower is deemed “vulnerable,” the next steps follow:

■ The debtor informs the agency that a foreclosure of the residence is imminent.

■ The agency intervenes in the auction and acquires the property without competition at a price up to 30% lower than the starting bid.

■ The debtor remains in the home as a tenant, paying a standard rent determined by ministerial criteria, while also receiving a state subsidy of €70–210 per month.

■ The stay in the property is set at twelve years. The tenant has the right, if they recover financially, to repurchase the property at the end of the 12-year period.

The right of repurchase

The most “optimistic” aspect of the new tool lies in the right of repurchase granted to the tenant. If the household’s financial situation improves within the twelve-year period, the debtor can regain ownership of the home.

This right is also transferable to heirs, strengthening the sense of security for future generations, within a framework of justice and transparency.

At the same time, the state supports the scheme to prevent evictions: during the transitional phase, the Interim State Support Program operates, providing a monthly state contribution of €70–210 (depending on household composition) for 15 months and suspending enforcement measures (e.g., foreclosures/evictions) for primary residences. This interim framework will conclude with the establishment of the agency.

The role of banks and investors

Four leading international investors (Bain Capital, Fortress, Christofferson, Resolute Cepal) are participating in the tender and are invited to submit binding offers by February 26, 2026. The agency will operate on private-sector criteria, without burdening the state budget beyond the предусмотрed social rent subsidy.

For financing the project, the four systemic banks intend to contribute a total of €100 million, which through leverage can be doubled to €200 million. The final contractor will also contribute capital, while banks will provide additional lending.

What is the benefit for participants? Beyond rental income and the option to resell the property after 12 years (to the debtor or a third party), the full range of options for managing non-performing loans is now completed (Property Agency for Vulnerable Debtors, out-of-court settlement or bilateral agreements for others). As the parameters “lock in” regarding who is protected—based on social justice and measurable rules—this will allow the liquidation of non-performing loans once the tender processes are completed, now entering their final stage.

Retroactive application

The circle of beneficiaries may expand even further if, as revealed today by THEMA, the measure is applied retroactively.

Specifically, according to information, the economic team is examining the possibility that immediately after the agency becomes operational, another significant intervention will be made: extending the measure to borrowers who have already lost their homes at auction because they were unable—due to ignorance or inability—to join the interim protection program.

Thus, if the property remains in a servicer’s portfolio or with a bank and has not passed to third parties, the agency will be able to purchase it retroactively, allowing the vulnerable individual to return and live in it as a subtenant, with the prospect of even regaining ownership.

Photo: EUROKINISSI

Ask me anything

Explore related questions