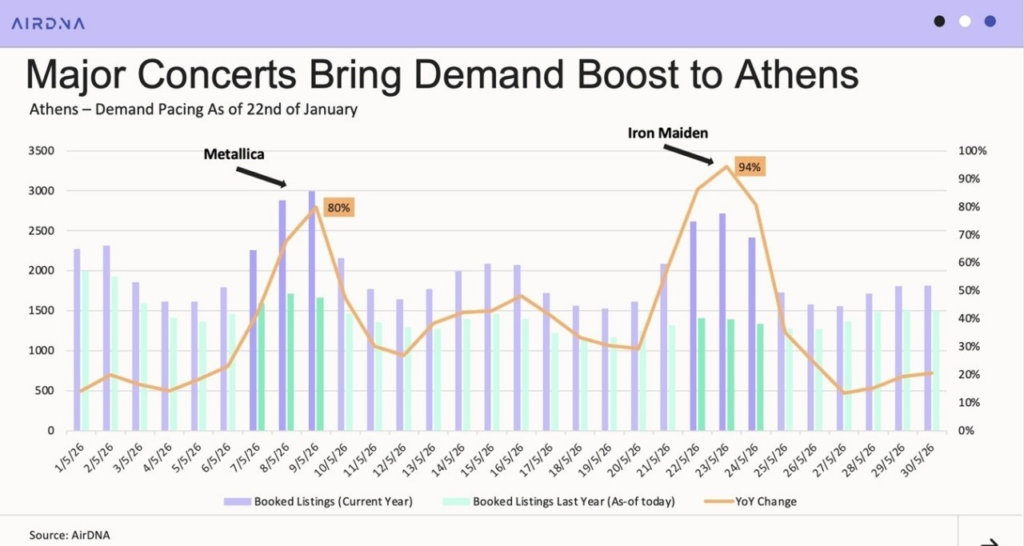

The staging of the big Iron Maiden and Metallica concerts next May have already boosted bookings for Athens at that time with daily increases of as much as +94% compared to 2025 for the day of one of the two concerts.

Figures from well-known short-term rental data analytics company (based on bookings up to 22 January 2026) AirDNA show exactly how the two major concert events are affecting traffic in Athens just before the start of summer: May starts with a +14% increase in bookings, a number that gradually rises to +80% compared to the same period last year on the date of Metallica’s first concert on Saturday 9 May, with an even bigger increase thereafter. On the day of the second concert, that of Iron Maiden on 23 May, the increase in bookings at Airbnb accommodation in Athens is +94% compared to the same period last year, a truly impressive figure for the Greek market.

Data Presented by Camilo Schmid Rivas, AirDNA Research Analyst, at the “Short Stay Conference Athens 2026”

Yesterday (February 19, 2026), Camilo Schmid Rivas, a research analyst at AirDNA, presented key data at the “Short Stay Conference Athens 2026,” a two-day event held on February 19–20. His presentation provided a detailed overview of the Greek short-term rental market’s trajectory, dynamics, supply, demand, performance, and outlook for 2026.

Outlook for 2026

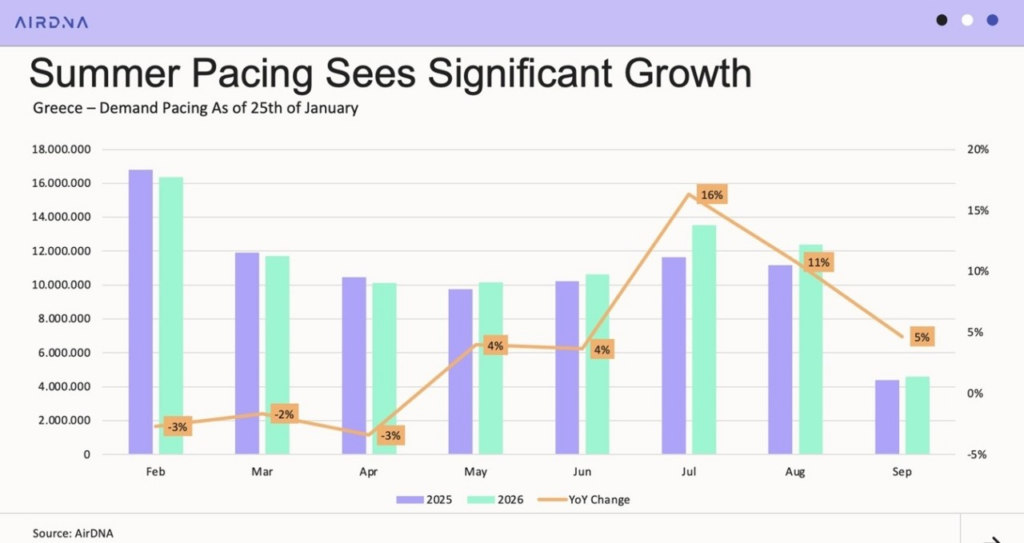

While it is still early in the year, initial indicators for the summer of 2026 are highly positive for Greece’s short-term rental market. Demand is already rising, particularly for July, which has seen a 16% increase in bookings compared to the same period last year. August is also up by 11%. May, June, and September show more modest growth, with increases of 4%, 4%, and 5% respectively (based on demand up to January 25). For the remainder of the winter and early spring, AirDNA reports a slight decline in demand, down by 2–3% compared to last year.

Regarding accommodation categories, AirDNA’s data for 2026 reveals that mid-range, upscale, and luxury properties are leading in popularity for the summer season, despite their higher prices. These categories are experiencing greater demand growth compared to budget accommodations.

Market Trends in 2025

During yesterday’s presentation, the AirDNA analyst highlighted Greece’s distinct path compared to other European markets. The supply of accommodations was minimally affected during the pandemic and recovered more quickly than in most European countries. Since 2023, while other Mediterranean markets have slowed, Greece has accelerated, now ranking as the sixth-largest short-term rental market in Europe, with over 130,000 active listings—surpassing Croatia. In 2025, supply reached a historic high of approximately 160,000 listings before the usual seasonal decline in the fourth quarter. However, growth has shifted from the explosive rise of 2024 to more moderate rates in 2025, partly due to new regulatory frameworks introduced last autumn. This slowdown is milder than in Spain, where mass delistings have occurred, and in Italy, where a temporary supply increase was observed due to the Winter Olympics. In terms of cities, Athens and Thessaloniki remain the main drivers of growth, with rising activity in areas such as Piraeus, Marousi, and Glyfada, as well as emerging island markets like Chios, Lesvos, and Kalymnos.

Demand strengthened significantly from the first to the third quarter of 2025, reaching a peak of nearly one million additional overnight stays compared to 2019. Travelers are now booking earlier, with 58% of all bookings for the period from June to September (down from 60% in 2019). Off-peak tourism has also grown, effectively extending the season to nine months, with March, May, and October accounting for 26% of total bookings in 2025, up from 22% in 2019.

AirDNA’s analysis notes that Greece remains heavily dependent on international demand, which accounts for about 90% of bookings. Demand from the US continues to rise, Germany maintains its momentum, while France shows a decline due to economic uncertainty.

The market structure is still dominated by small units, with studios and one-bedroom apartments making up the majority of listings. There is a balance between apartments and villas, but new listings are being added with greater caution. AirDNA data indicates that review ratings tend to decrease as portfolio size increases. Property managers are competitive in terms of location, but there is a perceived lag in value, reflecting higher guest expectations for professionally managed properties.

Occupancy rates in the summer of 2025 remained stable compared to 2024, but were still 7.8% higher than in 2019. Mid-range properties proved the most resilient last year, while luxury accommodations outperformed at the European level. Corfu and Crete saw increases in both occupancy and average daily rate (ADR), while Athens and Mykonos experienced a slowdown, with Mykonos recording a significant 15% correction in ADR to €361. In Athens, the average rate slightly decreased to just under €58, down from €60 in 2024.

Ask me anything

Explore related questions